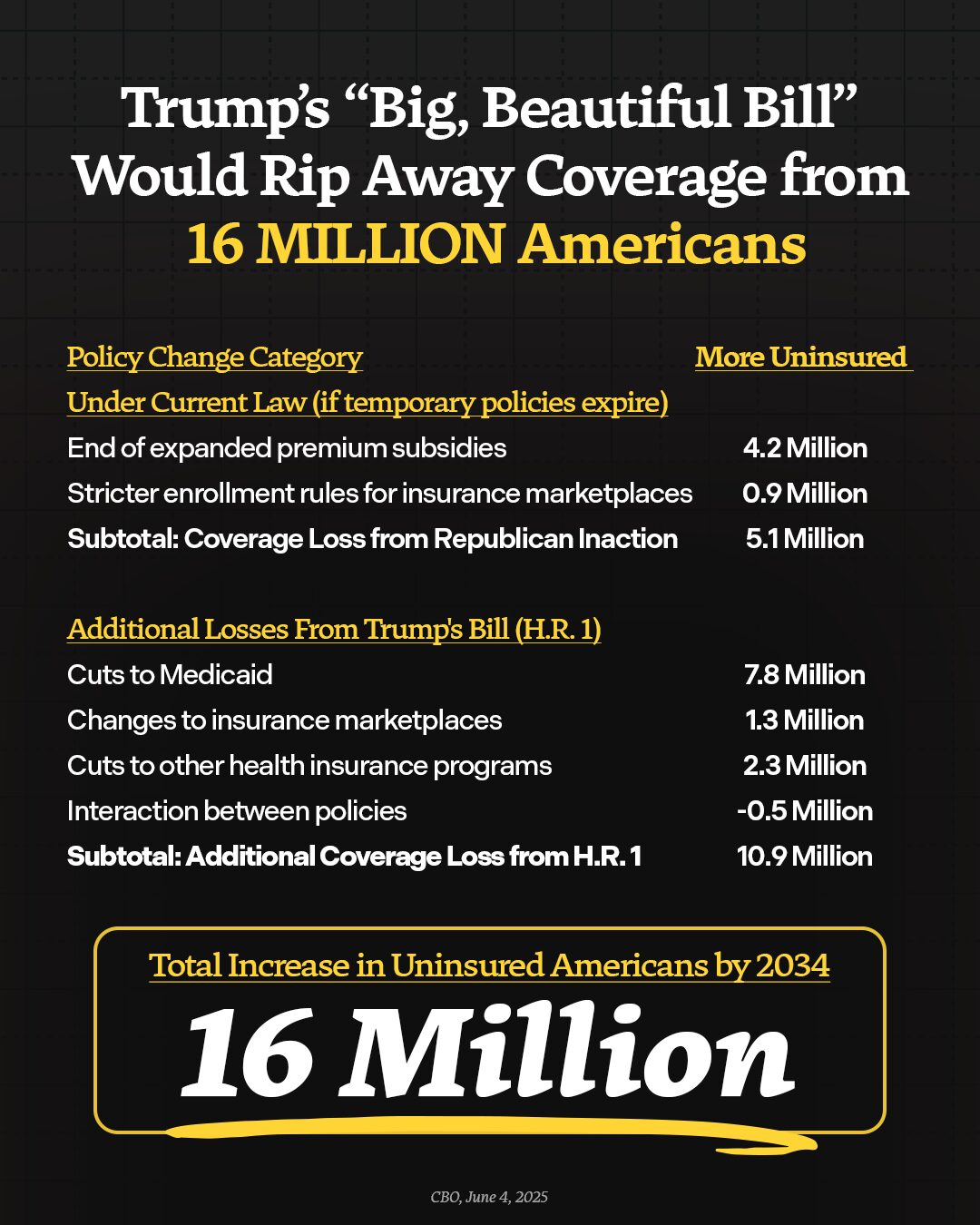

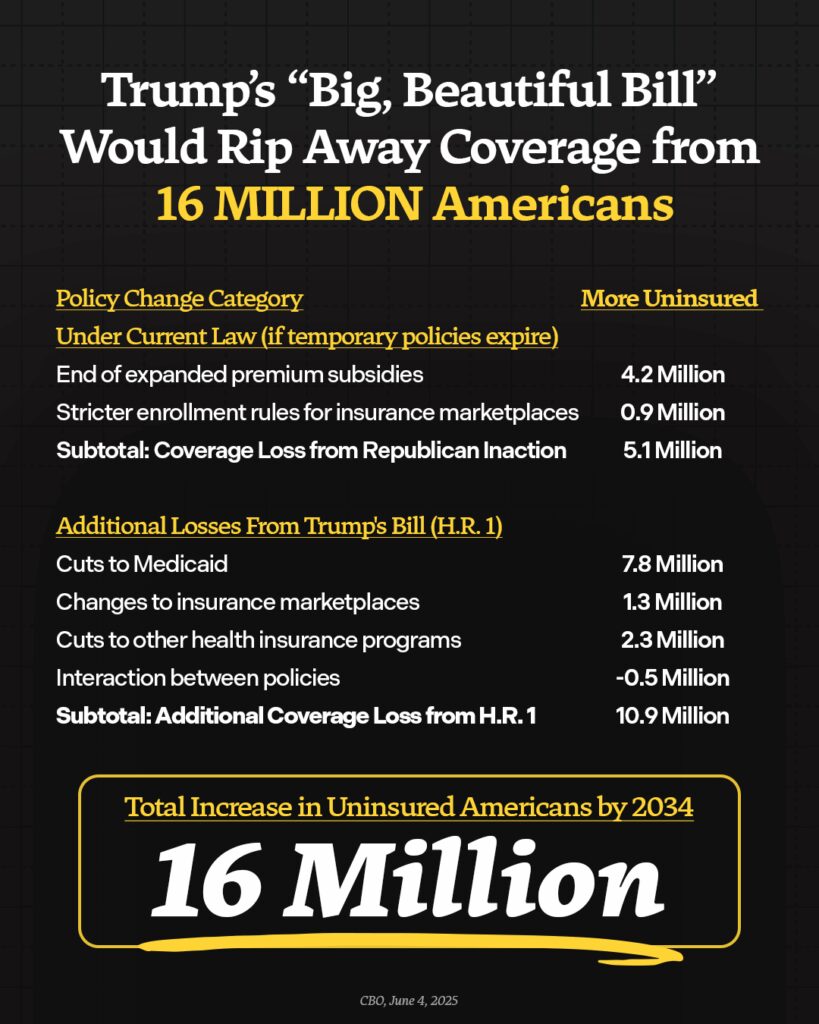

Over A Quarter Of Nursing Homes Will Be Forced To Close Under The GOP Bill

Republicans are charging through the Senate with their reconciliation bill, which makes the largest cuts to health care in American history—including billions in critical funding for nursing homes. These Republican cuts will force more than a quarter of nursing homes to close their doors. If Senate Republicans are successful in passing the bill, millions of Americans will lose their access to care, kicking seniors in nursing homes to the curb, shuttering rural hospitals, and forcing people to travel further and wait longer for lifesaving care. By closing care facilities across the country, the GOP bill will not only rip care away from seniors, people with disabilities, and hard-working families across the country—thousands will lose their jobs and local economies would suffer. Families will be forced to choose between getting their loved one the care they need and putting food on the table, sick people will go without care, and people will die. The Republican big, ugly tax scam will kick 16 million Americans off their health care, cut Medicare, and throw our entire health care system into chaos.

By The Numbers:

- Medicaid pays for over six in ten (63%) residents in nursing homes. Without this care, seniors and people with disabilities will be left without the assistance they need for basic activities such as bathing, dressing, and walking.

- Medicaid is the largest payer of long-term care in America. Medicaid paid for 44 percent of the $147 billion spent on institutional long-term care in 2023.

- The GOP is proposing $800 billion in Medicaid cuts at a time when 80 percent of nursing homes are on the brink of closure. These cuts would force more than a quarter of nursing homes to close their doors.

- GOP Medicaid cuts will undermine the care workforce. More than half of nursing homes would be forced to cut staff at a time they are already facing widespread shortages. An estimated 477,000 health workers will lose their jobs as a result of GOP cuts to Medicaid, from nurses to physical therapists.

How GOP Policies Will Hurt Nursing Homes, Seniors, and Americans With Disabilities

- More Than A Quarter Of Nursing Homes Across The Country Will Be Forced To Close Their Doors. 774 nursing homes have already closed since the pandemic, displacing over 28,000 residents and leaving 40 additional U.S. counties without nursing home care. GOP cuts to Medicaid will exacerbate the nationwide nursing home shortage, forcing more than a quarter of U.S. nursing homes to close their doors and leaving numerous Americans without options for their loved ones’ care at time when 57 percent of nursing homes already have a waitlist for new residents.

- Seniors and People With Disabilities Will Be Kicked To Curb. The Congressional Budget Office estimates at least 1.3 million seniors and people with disabilities will lose Medicaid due to GOP proposals, leaving them without coverage for long-term care. Republicans are pushing for the largest cuts to Medicaid in history which will also force states to cut back on the services they cover and potentially limit seniors’ access to nursing home care. The $800 billion in proposed cuts to the federal Medicaid budget is equivalent to 72 percent of federal funding for long-term care. Policies such as provider tax and state-directed payment restrictions will also make it harder and harder for states to financially support long-term care for a rapidly aging population with the number of adults over age 85 expected to more than double by 2040.

- Families Will Go Into Debt Struggling To Afford Care For A Loved One. Since Medicare generally does not cover long-term care, families will be left without affordable options for long-term care for their moms, dads, and grandparents. The average cost of a nursing home is over $111,000 a year – a price tag out of reach for most families without assistance. Families who need help may be forced to go into financial debt to get their loved ones the care they need. Third Way estimates GOP proposals will push at least 5.4 million Americans into medical debt and result in $50 billion increase in total medical debt. Families who cannot afford more debt will be forced to cut back on their hours, quit their jobs, or make other sacrifices to look after their loved one.

- The Already Struggling Care Workforce Will Be Devastated. Nursing homes across the country are already struggling with staffing shortages that can lead to poor quality of care. CMS estimates nursing facilities are nearly 80,000 short of the workers they need to provide adequate care. In 2024, 20 percent of nursing homes closed a unit, wing, or floor due to labor shortages. According to a recent survey from the American Health Care Association, more than half of nursing homes will be forced to cut staff due to GOP cuts to Medicaid. Nursing homes employ over 1.4 million Americans and 30 percent of direct care workers rely on Medicaid themselves for their health care and would be in danger of losing their coverage.