Protect Our Care Blasts Alex Azar Confirmation as HHS Secretary News Protect Our Care Blasts Alex Azar Confirmation as HHS Secretary Washington, DC - After the Senate voted to confirm Alex Azar as the Trump Administration’s…ashoupJanuary 24, 2018

Republicans Must Finally Confront Trump’s Disastrous Handling of Opioid Crisis News Republicans Must Finally Confront Trump’s Disastrous Handling of Opioid Crisis Inaction + Funding Cuts = Sabotage Washington, DC - After former Congressman Patrick Kennedy, a…ashoupJanuary 23, 2018

New Washington Post/ABC News Poll: Health Care Remains Top Concern for Voters NewsStories New Washington Post/ABC News Poll: Health Care Remains Top Concern for Voters A new Washington Post/ABC News poll asked Americans about the policies which took precedent during…ashoupJanuary 22, 2018

President Trump’s First Year: A War on Women’s Health News President Trump’s First Year: A War on Women’s Health TO: Interested parties FROM: Marjorie Connolly, Communications Director, Protect Our Care RE: President Trump’s First…ashoupJanuary 19, 2018

Trump Administration Breaks Its Promise Again on Opioid Crisis News Trump Administration Breaks Its Promise Again on Opioid Crisis Following today’s news that the Trump Administration will propose a 95% cut to the Office…ashoupJanuary 19, 2018

This Week in the War on Health Care — January 15-19, 2018 News This Week in the War on Health Care — January 15-19, 2018 The week, as much of the focus in Washington shifted to DACA and negotiations in…ashoupJanuary 18, 2018

CR Proposal Shows Republicans Remain Obsessed with ACA Repeal at the American People’s Expense NewsStories CR Proposal Shows Republicans Remain Obsessed with ACA Repeal at the American People’s Expense Washington, DC - After Congressional Republicans released a Continuing Resolution proposal that takes aim at…ashoupJanuary 17, 2018

Enough is Enough: the Trump Administration’s Sabotage of Our Health Care Must Stop NewsStories Enough is Enough: the Trump Administration’s Sabotage of Our Health Care Must Stop To: Interested Parties From: Brad Woodhouse, Campaign Director, Protect Our Care Subject: Enough is Enough:…ashoupJanuary 16, 2018

Health Care As A Defining Issue Of 2018 StoriesNews Health Care As A Defining Issue Of 2018 To: Interested Parties From: Geoffery Garin Subject: Health Care As A Defining Issue Of 2018…ashoupJanuary 16, 2018

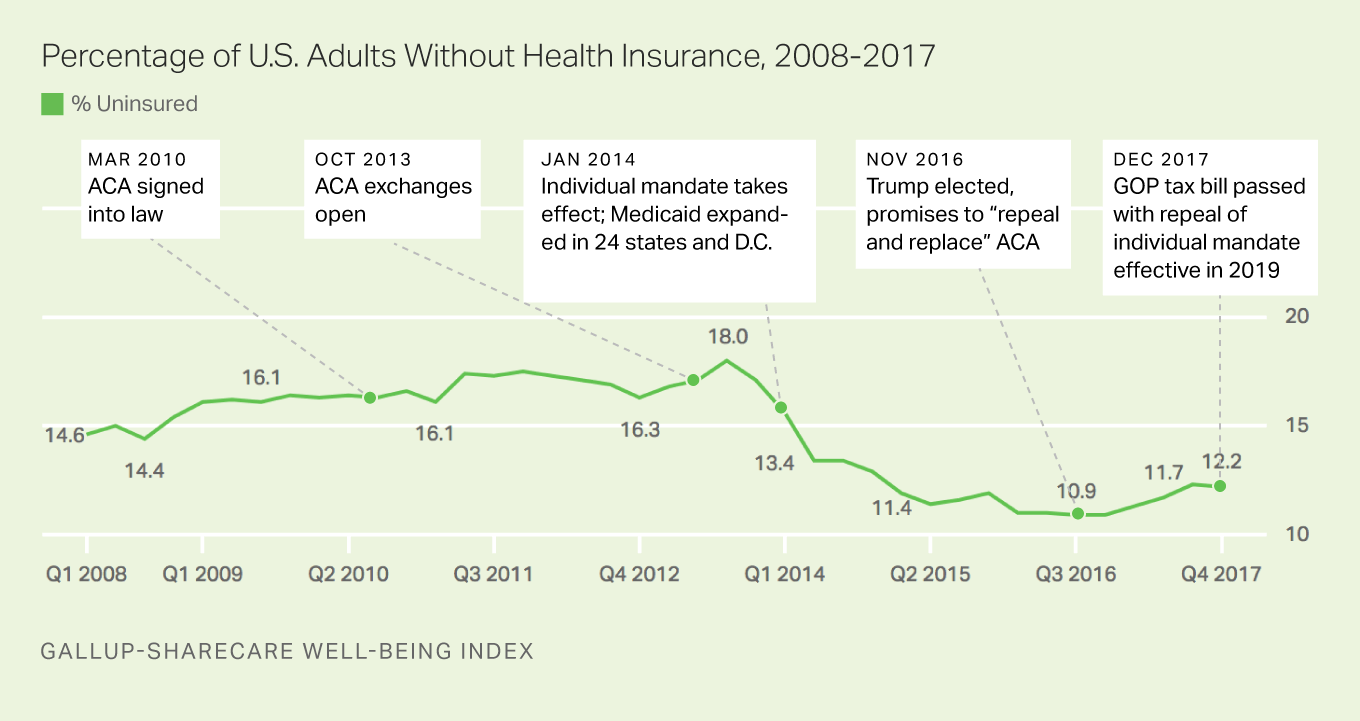

Gallup Poll: Uninsured Rate Rose in Trump’s First Year News Gallup Poll: Uninsured Rate Rose in Trump’s First Year After a new Gallup poll showed that America’s uninsured rate jumped during Trump’s first year…ashoupJanuary 16, 2018