Based on what we know so far, the reviews of Trump’s health care sabotage Executive Order aren’t pretty.

In fact, they’re downright scary.

President Trump’s pledge to sign an Executive Order later this week will sabotage health care, achieving his dream of health care repeal that failed with bipartisan opposition in Congress and overwhelming opposition from the American people.

Trump has been rooting for health care to fail, saying “Let it be a disaster,” and his sabotage will end protections for those with pre-existing conditions, raise health care premiums and deny access to coverage for millions of Americans — and could result in the collapse of the individual insurance market.

But don’t take our word for it.

Look at the early reviews that have exposed the truth…

Larry Levitt, Kaiser Family Foundation: “If the executive order is as expansive as it sounds, it could severely destabilize the individual and small business insurance markets. Association plans exempt from the ACA can cherry pick healthy people and make coverage unaffordable for those with pre-existing conditions. If loosely regulated association plans are allowed, insurers will leave the ACA marketplaces as soon as they can or hike premiums a lot.”

Larry Levitt, Kaiser Family Foundation: “The executive order also reportedly envisions expanding the use of short-term health insurance plans. Short-term insurance plans can offer inexpensive coverage to currently healthy people, but they exclude people with pre-existing conditions. If healthy people can enroll in short-term plans and avoid the individual mandate penalty, the ACA marketplaces could collapse. Anything that creates a parallel insurance market for healthy people will lead to unaffordable coverage for sick people. Middle class people with pre-existing conditions ineligible for ACA subsidies could be especially vulnerable under the executive order. You can bet this executive order will get challenged in court, but it could also create lots of confusion going into open enrollment.”

Cori Uccello, American Academy of Actuaries: “Cori Uccello, senior health fellow at the American Academy of Actuaries, said that one aspect to watch in the order is when the changes will take effect. Insurers have already set their prices and made plans for 2018. ‘Anything that applied to 2018 would be incredibly destabilizing,’ she said. ‘It would still be destabilizing in 2019 but people would know ahead of time.’”

Matt Fiedler, Brookings Institute: “‘Associations would siphon many healthier people out of the ACA-compliant market, driving up premiums,’ said Matt Fiedler, a fellow with the Center for Health Policy at Brookings Institute. ‘Higher premiums in the ACA-compliant market would result in big cost increases for many sicker enrollees — since they would not have the option of switching to the association market — and likely for the federal government as well.’”

Joseph Antos, American Enterprise Institute: “Joseph Antos, a health policy scholar at the conservative American Enterprise Institute, agrees. ‘Trying to exempt these new associations from ACA rules that apply to all other plans doesn’t strike me as something that’s going to stand up in federal court,’ Antos says.”

National Association of Insurance Commissioners: “AHPs would fragment and destabilize the small group market, resulting in higher premiums for many small businesses. … AHPs would be exempt from state solvency requirements, patient protections, and oversight exposing consumers to significant harm.”

Commonwealth Fund: “If they do so, the health insurance sold via the AHP could become exempt from consumer protections such as the essential health benefits standard and the prohibition on charging higher premiums to people with preexisting conditions. The result would be increased risk for higher premiums and fewer plan options on the individual market, as well as fraud and insolvency.”

Craig Garthwaite, Northwestern University: “‘There’s a general belief that at every turn the federal government is going to create regulations to hurt rather than help the markets,’ said Craig Garthwaite, director of the health care program at Northwestern University’s Kellogg School of Management, referring to the Trump administration. ‘It unwinds the ability of people with pre-existing conditions to get insurance under the ACA,’ Garthwaite said.”

Gary Claxton, Kaiser Family Foundation: “‘If the market’s already fragile right now, this is going to make it much more fragile,’ said Gary Claxton, director of the health-care marketplace project at the Kaiser Family Foundation. ‘All of this would be the start of the end of the individual ACA market.’”

Linda Blumberg, Urban Institute: “‘The risks of trying to do the kinds of things we’re hearing about are really tremendous,’ said Linda Blumberg, senior fellow at the Health Policy Center at the Urban Institute.”

Associated Press: “Without those healthy customers, the cost might rise faster for people with medical conditions.”

The Hill: “President Trump’s planned executive order on ObamaCare is worrying supporters of the law and insurers, who fear it could undermine the stability of ObamaCare.”

Washington Post: “If at first you don’t succeed at repealing Obamacare, try, try again — with an executive order. President Trump, desperate for a health-care win that Congress couldn’t hand him, is pursuing a backdoor way of letting more Americans buy insurance plans free of the Obamacare regulations that Republicans have blamed for big premium hikes and costly deductibles.”

Washington Examiner: “Both association health plans and short-term plans are less expensive than Obamacare plans because they offer limited coverage. They don’t guarantee same-cost coverage, or any coverage, for people with pre-existing illnesses and they do not cover a broad range of medical care, from addiction treatment to maternity care.”

Recent reports and the opinions of experts indicate that President Trump will announce an Executive Order this week designed to sabotage the health care system and achieve some of the GOP’s health care repeal goals that have failed to pass in Congress and which have been rejected overwhelmingly by the American people. Trump’s sabotage will raise health care premiums, deny access to health care for millions of Americans and could result in the collapse of the individual insurance market.

According to experts, the Executive Order is expected to:

Destabilize the health insurance marketplace

Inject significant uncertainty in the health insurance marketplace just weeks before the start of the already-shortened open enrollment period

Increase costs for millions

Gut protections for people with pre-existing conditions, making coverage for them unaffordable

Return power to insurance companies, who would be able to charge more for less care, including selling policies that don’t cover necessary care

Undermine the ability of state insurance commissioners to effectively regulate and rein in insurance companies

In response to this latest secret, partisan repeal effort undertaken without any input from experts, Protect Our Care Campaign Director Brad Woodhouse released the following statement:

“President Trump has gone from failing at repeal to flailing with sabotage, and the victim is our health care,” said Woodhouse. “This Executive Order is nothing but the latest, and most damaging, in a series of attempts to sabotage our health care by this administration. From the President’s order to dismantle the health care law on his first day in office to forcing rate hikes by threatening to cancel required payments, the Trump Administration isn’t filled with health care solutions; it’s filled with health care saboteurs.

“After bipartisan majorities in Congress and the overwhelming majority of the American people rejected his health care repeal, President Trump is still attempting to dismantle our health care out of vengeance.

“Republicans in Congress cannot sit by idly and let this happen. The GOP must stand up to this sabotage and force the Administration to protect and strengthen our health care, rather than let them play politics with people’s lives.”

NEW REPORT: VAST MAJORITY OF STATES ATTRIBUTE HEALTH INSURANCE RATE INCREASES TO TRUMP SABOTAGE

The deadline for states to finalize premium rates for the individual and small group market and submit them to the federal government for approval was one week ago (9/27/17) and many states have publicly announced double-digit increases.

In a comprehensive review of all the 28 states whose final state-approved rates that have been made public, this new report from Protect Our Care shows that the vast majority — 20 states — attribute their rate increases in part to the Trump administration’s sabotage of our health care. Blame for the increase was squarely placed on the Trump administration and Republicans in Congress injecting uncertainty into the marketplace by threatening to default on cost-sharing reduction (CSR) payments that help lower out-of-pocket costs in some way, shape or form.

Our analysis finds:

20 states attribute rate increases to uncertainty over whether the Trump administration will make CSR payments: Connecticut, Florida, Georgia, Idaho, Illinois, Indiana, Louisiana, Maine, Michigan, Mississippi, New Mexico, New York, Ohio, Oregon, South Carolina, South Dakota, Tennessee, Utah, Virginia and Washington. (Oregon cited weakening enforcement of the individual mandate for some of its rate increase.)

Five states indicated their state increases would be even higher if they assumed the Trump administration would not be making the CSR payments: Arizona, Arkansas, Colorado, Maryland and Vermont.

Two states — Alaska and Minnesota — have mostly cut their insurance rates next year after the federal government allowed them to start a new reinsurance program.

One state, Nevada, did not release any reason for their 2018 rates.

While they’re not included in this analysis of rates, the sabotage has had other consequences including insurers that decided not to participate in the marketplace next year, citing the uncertainty the Trump administration had created. Anthem in Maine announced it was exiting the marketplace at the last minute, as well as Medica in North Dakota, to name a couple of examples.

We now have the clearest evidence yet that the Trump administration’s sabotage of our health care system is leading to the higher insurance rates we are seeing for 2018.

Prior to the Trump administration, independent analyses show that the Affordable Care Act was working. Standard’s & Poor said it expected insurers’ performance in the marketplaces to be better in 2016 than in 2015, and 2017 would be better than 2016. The nonpartisan Congressional Budget Office said it anticipated “the market to be stable” under the ACA. The average premium after tax credits increased by $1 dollar, from $100 in 2016 to $101 in 2017.

Evidence is Clear: States Blame Uncertainty for Even Higher Rates

Associated Press: “Jeff Stelnik, the [BCBS of AZ]’s senior vice president of strategy, sales and marketing, told The Associated Press the change came because of improved profitability on current plans and an assumption that the federal government will continue funding a program reducing some customer costs. The decision comes despite worries from many insurers that the “cost sharing reductions” they are required to offer many lower-income customers won’t be funded by the Trump Administration. ‘There still continues to be uncertainty in the marketplace, we still continue to be concerned by that uncertainty,’ Stelnik said. But he said a deadline for finalizing premiums for 2018 and a better balance between premiums and claims ‘enabled us to be confident in the new pricing that we are putting in the marketplace.’”

[Note: Insurers updated their rate requests on August 21 that reflected higher rates assuming no CSR payments. The state-approved rates are more aligned with the earlier requests.]

Colorado Division of Insurance: “In Colorado, premiums for individual plans (not from an employer) will be increasing by an average of 26.7 percent…The premiums would be up to 14 percent higher if we used the non-CSR-funded premium requests.”

Connecticut Insurance Department: “The federal funding of the CSR payments for coverage year 2018 would have reduced the approved rate increases from 27.7% to 16.8% for [ConnectiCare Benefits Inc] and from 31.7% to 24.7% for Anthem.”

“As a result of the lack of clarity about future funding of CSRs and the need to make rate determinations for 2018, the Department asked exchange carriers to make a supplemental filing which assumed CSRs would not be paid. The supplemental rate increase for non-payment of the CSRs is 16.7 percent, this is applied only to the Silver exchange plans. The increase in rates for the Silver exchange plans will be mitigated for consumers receiving tax credits by the increase in the federal tax credits for 2018.”

Miami Herald: “Florida regulators said most of the average rate hike — 31 percentage points [of the 44.7 percent total] — came from standard plans sold on the ACA exchange at Healthcare.gov. Insurers raised rates for those plans due to the political uncertainty that has plagued the healthcare debate, specifically whether the Trump administration will stop paying subsidies that lower out-of-pocket costs for low-income Americans.”

Atlanta Journal-Constitution: “Every single one of the four companies offering policies on the exchange here plans to raise their rates by an average of more than 50 percent, if Washington does not give certainty on the subsidy funding.”

Idaho Statesman: “‘The rate increases, in particular on silver-level plans, are definitely greater than we would like,’ said Idaho Department of Insurance Director Dean Cameron. ‘There is legitimate uncertainty” regarding whether the government will continue to pay for certain subsidies for low-income users of the exchange….The rates that insurers are slated to charge for “silver” plans next year would be cut by more than 20 percent if subsidies are continued, according to the Idaho Department of Insurance. And that would affect how much actual help consumers would get to pay for those pricey “gold” plans.”

Illinois Department of Insurance: “‘DOI is committed to ensuring that consumers are prevented from incurring higher health insurance costs due to uncertainty in Washington,’ said DOI Director Jennifer Hammer. ‘Insurers have been advised to apply the CSR uncertainty cost, solely to silver plans.’ This change makes it important that consumers diligently shop for a plan this year. DOI reminds consumers that cost alone may not be the only factor to consider when selecting a plan. For example, consumers may want to also consider a plan’s provider network.”

ABC 6 News: “University of Indianapolis’ Director of Public Health programs, Heidi Hancher-Rauch, said ‘uncertainty’ is the reason for rising costs. ‘Insurance companies are left trying to figure out, OK, if we aren’t going to get that money from the government, how are we going to make up that difference,’ said Hancher-Rauch. Another uncertainty is whether the requirement for everyone to get insurance will be enforced. ‘We rely on those healthy people who are paying into the plans to do that cost sharing among all of us,’ said Hancher-Rauch. ‘We absolutely need those healthy people paying into the insurance to help offset some of those costs for the older and sicker individuals.’”

Greater Baton Rouge Business Report: “Both Vantage and Blue Cross announced earlier this summer they would raise rates by double digits for those who buy insurance through the ACA exchanges. Vantage raised such rates by upwards of 30%, while Blue Cross increased rates by 18.5%.

The companies said the major driver of the rate increase was uncertainty over cost-sharing reductions, which are designed to help insurance companies offer affordable coverage to low-income people. President Donald Trump’s administration has threatened to stop paying the subsidies. Vantage and Blue Cross also cited a lax enforcement of the individual mandate, the provision of the ACA that requires everybody have insurance.”

Maine Public Radio: “Maine’s Insurance Superintendent Eric Cioppa approved rate increases that range from 20 to 37 percent if the cost-sharing payments end.”

Maryland Insurance Administration: “The rates do not include any factor based upon the political uncertainty of future cost-sharing reduction payments.”

Michigan Department of Insurance and Financial Services: The size of the increases this year is partially due to the uncertainty as to whether the federal government will continue to fund Cost Sharing Reduction (CSR) payments. Under the Affordable Care Act (ACA), insurers on the Marketplace are required to provide financial assistance under plans covering individuals up to 250% of the federal poverty level and eligible American Indians. The CSR payments allow insurers to meet that legal obligation without increasing rates. The President has indicated he does not support these payments, and the federal government is currently making them on a month-to-month basis.

Wall Street Journal: “Mississippi’s insurance commissioner, Mike Chaney, said he is approving a 47.4% average premium increase for the state’s one ACA exchange insurer, which would have been around 17.9% if the cost-sharing payments were guaranteed. The insurer couldn’t bear the potential extra expense of funding the cost-sharing subsidies without the bigger premium bump, he said: ‘They can’t take that, they just can’t do it.’”

Albuquerque Journal: “The state’s top insurance regulator said the rate increases in 2018 are heavily influenced by uncertainty about whether the federal government will block or discontinue payments to insurers. President Donald Trump has repeatedly threatened to halt these reimbursements to insurance companies in his drive to dismantle the Affordable Care Act, as Obamacare is formally known.”

New York Times: “In New Mexico, the average rate increase for plans sold on the state marketplace is about 30 percent. ‘Half of that increase is due to the uncertainty in Washington and the inability to lead,’ said John G. Franchini, the state insurance regulator. The four insurers selling policies in the state marketplace are offering more types of plans.

ODI: “In addition, the average cost of coverage for individual plans sold on the federal exchange in 2018 will be 34 percent higher than the average cost of coverage in 2017. Approximately 11 percent of that increase is attributable to the assumption that insurers will not receive Cost Sharing Reduction (CSR) payments in 2018.”

Kaiser Foundation Health Plan of the Northwest — 14.8 %

Moda Health Plan — 4.7 %

PacificSource Health Plan — 2.8 %

Providence Health Plan — 10.8 %

Oregon Department of Consumer and Business Services: “Reasons for the rate changes include: The new Oregon Reinsurance Program. This program reduced individual market rates by 6 percent, and added a 1.5 percent increase to the small group market. Federal weakening of the individual mandate enforcement. This increased rates by 2.4 percent and 5.1 percent.”

Charlotte Observer: “A ‘cost sharing reduction’ subsidy reduces the amount that patients pay for deductibles and copays. About 20 percent of the 31 percent increase in premiums for S.C. residents is attributed to the uncertainty of funding for that subsidy, said S.C. Department of Insurance Commissioner Ray Farmer.”

Argus Leader: “But insurance executives said political efforts to reform healthcare created the uncertainty that drove prices up in the first place.

Assuming President Donald Trump doesn’t move to eliminate cost-sharing reductions, policyholders will see a 7.5 percent bump under Sanford and 17 percent under Avera, executives from each group confirmed.”

The Tennessean: “Uncertainty — wrought by the ongoing debate over Obamacare repeal-and-replace legislation and decisions by the White House and HHS officials — have clouded the premium request process, and led to higher requests. Cost-sharing reductions, a subsidy that offsets out-of-pocket costs for some shoppers, are divisive in Washington, D.C. There is no long-term commitment that CSRs will be paid to insurers, and the decision is being made monthly. BCBST attributes nearly all of its average 21 percent premium increase request to the unknowns of the upcoming year.”

TDCI Commissioner McPeak: “Instead, it appears more likely that Tennesseans must prepare themselves for a round of actuarially justified rates for 2018 that are far higher than could be necessary as a result of uncertainty in Washington. On behalf of Tennessee consumers, I continue to urge Congress to take action to stabilize insurance markets. The Department stands ready to take action to aid consumers should stabilization measures be enacted.”

Deseret News: “Just the general increase in medical trends that we’ve seen over the past decade — as the cost of services increase, premiums increase,” [Utah Insurance Department spokesman Steve] Gooch said. ‘There’s (also) an increase due to the uncertainty over whether the (cost-sharing payments) will be funded. So that causes some uncertainty in the risk profile, so that’s kind of built into those (new) rates.’”

Addison County Independent: “If the cost sharing reduction payments were not continued, BCBS [which has 87 percent of the market] estimates premiums would go up by an additional 1.5 to 2 percent.”

Richmond Times-Dispatch: “As many see their options for health plans dwindle down to one insurer, premiums are simultaneously set to rise by an average of 57.7 % next year in Virginia’s individual marketplace…‘The rate increases can be attributed to an unstable market, with too few healthy people signing up to balance out the number of sick people who enroll, and the uncertainty of cost-sharing reduction payments, which are meant to go to insurers to cover the cost of offering lower prices to poor members, but which the federal government has refused to guarantee.’”

Washington Health Benefit Exchange Board: “Rates for the health plans certified represent a 24 percent increase over those available through the Exchange for 2017 coverage…However, should the federal government stop funding CSRs at some point in 2018, the OIC has determined that they may legally adjust the original lower rate to the approved higher rates of silver plans in the Exchange.”

Anthem Cites Uncertainty over Cost-Sharing Reduction Payments, which President Trump Has Threatened to Cancel, Among other Reasons, in Decision to Leave Market

WASHINGTON, D.C. — Today, one day after the failure of GOP’s latest iteration of a partisan repeal bill which would have thrown the country’s health care system into chaos, the effects of President Trump’s intentional sabotage of health care were once again made clear when Anthem announced it would exit Maine’s individual insurance market next year. Why?

“‘A stable insurance market is dependent on products that create value for consumers through the broad spreading of risk and a known set of conditions upon which rates can be developed,’ said Anthem spokesman Colin Manning in a statement. ‘Today, planning and pricing for ACA-compliant health plans has become increasingly difficult due to a shrinking and deteriorating individual market, as well as continual changes and uncertainty in federal operations, rules and guidance, including the restoration of the health insurance tax on fully insured coverage and continued uncertainty around the future of cost sharing reduction subsidies.’”

As the Portland Press-Herald noted, however, actions taken by Congress — like the payment of cost-sharing reductions — could potentially bring Anthem back into the marketplace:

“Manning did not close the door on returning to the Maine marketplace if conditions stabilized. There are proposals in Congress to mandate that the cost-sharing reduction funding be paid to insurers, and other measures to stabilize the marketplace. ‘Our commitment to members has always been to provide greater access to affordable, quality healthcare, and we will continue to advocate solutions that will stabilize the market. As the marketplace continues to evolve and adjust to changing regulatory requirements and marketplace conditions, we will reevaluate whether a more robust presence in the exchange is appropriate in the future.’”

In response, Protect Our Care Campaign Director Brad Woodhouse issued the following statement:

“Anthem’s decision to pull out of Maine is the direct consequence of uncertainty created in the marketplace by Republicans pushing for partisan repeal of our health care and President Trump’s intentional efforts to sabotage the law,” said Woodhouse. “President Trump has been playing politics with cost-sharing reduction payments by continually threatening to cancel them even though they lower out-of-pocket costs for millions of Americans. This uncertainty has led to decisions like Anthem’s.

“President Trump and Republicans who have cheered him on and supported repeal are intentionally harming people’s health care for sheer politics. The American people know this and they will hold them accountable for undermining the health care of the American people. Instead of sabotaging America’s health care, Republicans should follow the example of Senator Susan Collins, who has called for Democrats and Republicans to work together to improve health care for the American people.”

Analysts Agree: Every State Loses Under Graham-Cassidy Affecting People’s Care. Multipleindependentanalyses — and even Trump’s own CMS — agree that states would be worse off if theGraham-Cassidy repeal bill passess. Over time, every state loses because Graham-Cassidy zeroes out its block grants and ratchets down its spending on the Medicaid per capita cap. This means people would not have access to the financial assistance to help lower their health care bills, and federal Medicaid funding would no longer adjust for public health emergencies, prescription drug or other cost spikes, or other unexpected increases in need.

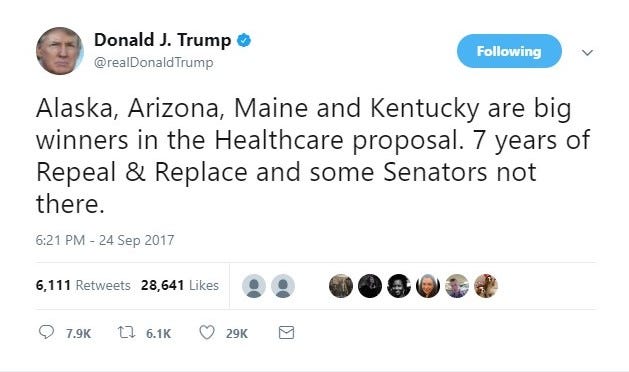

Alaska stands to lose $2 billion from 2020–2027 and $14 billion over the next two decades.

Arizona stands to lose $19 billion from 2020–2027 and $133 billion over the next two decades.

Maine stands to lose $2 billion from 2020–2027 and $17 billion over the next two decades.

Kentucky stands to lose $11 billion from 2020–2027 and $81 billion over the next two decades.

And according to an AARP analysis, the bill’s age tax would lead to huge increases in total costs for a 60-year-old making $25,000 in each of these states:

The Kaiser Family Foundation now confirms that 3,006 of the 3,007 counties in the United States have Affordable Care Act marketplace plans for next year. The one county that doesn’t, Ohio’s Paulding County, serves 334 people.

Republicans keep saying that many people will not have access to health care plans and make discredited claims about a non-existent death spiral. The claims have been debunked by the nonpartisan Congressional Budget Office and now by the facts in the 2018 coverage map from Kaiser Family Foundation.

Unfortunately, that hasn’t stopped the lies. Just last night, GOP Speaker Paul Ryan again made these debunked claims.

CBO: 20–25 Percent Premium Increase, Nearly $200 Billion Cost to Taxpayers, Coverage Losses, Market Uncertainty If Trump’s Cancels Health Care Payments

While Republicans are in the midst of responding to the fallout from Donald Trump’s latest comments on the events in Charlottesville, soon they may have to answer for the President’s continued efforts to sabotage health care for the American people. Yesterday, the nonpartisan Congressional Budget Office confirmed that a decision by President Trump to cancel critical health care payments, known as Cost-Sharing-Reductions, would inject substantial uncertainty in the insurance markets, force premiums to increase by 20% next year and 25% by 2020 and increase costs to the taxpayer by nearly $200 billion over ten years.

The headlines on the CBO report are bad enough for Republicans, whose partisan repeal efforts, along with Trump’s bluster, have injected uncertainty into the health care marketplace. Imagine the fallout they will face if Trump follows through with his threat to cancel payments which lowers the cost of health care for millions of Americans.

How do Republicans get out of this box canyon they’ve marched themselves into? Oppose Trump’s irrational sabotage of health care and join in a bipartisan process to improve health care for the American people. If not, these headlines will only get worse.

Associated Press: CBO: Higher premiums if Trump halts Obamacare subsidies

NBC 11 Baltimore: CBO: Deficit would spike, premiums would rise if Trump ends Obamacare subsidies

USA Today: CBO: Ending Obamacare subsidies would raise premiums and the deficit

Protect Our Care Campaign Director Leslie Dach released the following statement after the nonpartisan Congressional Budget Office confirmed that a decision by President Trump to cancel critical health care payments, known as Cost-Sharing-Reductions, would inject substantial uncertaintyin the insurance markets, force premiums to increase by 20% next year and 25% by 2020 and increase costs to the taxpayer by nearly $200 billion over ten years.

“This is the latest confirmation that the Trump administration’s plans to sabotage our health care will hurt millions of middle class Americans — bringing substantial uncertainty to the health insurance markets and forcing even higher double digit premium hikes. President Trump seems to prefer playing political sabotage games over doing his job of lowering costs and improving our health care. Whether he tries to repeal health care by legislation or by sabotage it means higher costs and less coverage for American families — and he will be responsible for those results.

“It’s time for all Republicans in Congress to stand up to Trump’s sabotage agenda, work with Democrats and pass real market stabilization reforms to improve our health care system.”

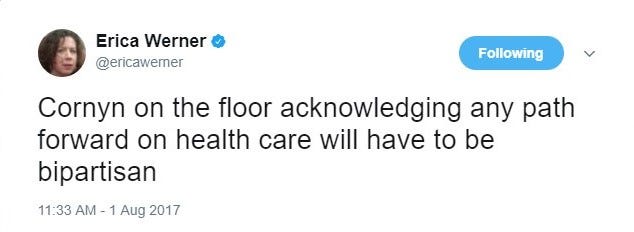

Despite President Trump’s twitter threats demanding the GOP continue with partisan repeal efforts, Republican Senators — including many in leadership — are acknowledging what the American people have said all along: it’s time to abandon partisan repeal. With the announcement from Sens. Lamar Alexander and Patty Murray that bipartisan hearings will begin the first week of September, it’s clear the only path forward on health care is a bipartisan one.

Sen. Orrin Hatch, Senate Finance Committee Chairman: “There’s just too much animosity and we’re too divided on healthcare… I think we ought to acknowledge that we can come back to healthcare afterwards but we need to move ahead on tax reform.”

Sen. John Thune, the third-ranking Republican: “Until somebody shows us a way to get that elusive 50th vote, I think it’s over.”

Sen. Roy Blunt, a member of GOP leadership: “Do I think we should stay on health care until we get it done? I think it’s time to move on to something else. Come back to health care when we’ve had more time to get beyond the moment we’re in and see if we can’t put some wins on the board.”

Seven in ten Americans want the Trump Administration and Congress to work across party lines to keep what works and fix what doesn’t in the current law. It’s time Republicans lived up to the promises they made and work with Democratic colleagues to improve our health care.

Angry at the failure of his partisan effort to repeal health care and because of his hatred for former President Obama, Trump is threatening to cancel payments that help lower people’s deductibles and other out-of-pocket costs. Who will pay the price? Everyday people trying to afford health coverage. Trump’s efforts to sabotage health care have already caused costs to go up. Now, his latest scheme will mean people will have to pay 19% more for their coverage, and could mean that insurance companies are forced to leave some parts of the country altogether.

Republican Members of Congress have recognized that there needs to be swift bipartisan action. Independent experts, business leaders, insurers and insurance commissioners all agree that Trump’s threat is putting at risk people’s health coverage. And the American public — 74 percent — wants Trump and his Administration to do what they can to make the law work — not continue to do what they can to make it fail.

Will Trump listen to his own party, experts and voters? Or will he ignore the facts and punish the American people?

IN RECENT DAYS, TRUMP HAS UPPED HIS THREATS TO DESTABILIZE THE INDIVIDUAL MARKET IN RETALIATION FOR THE SENATE’S FAILED BID TO REPEAL HEALTH CARE

HOWEVER, TRUMP’S STANCE IS THE OPPOSITE OF A NUMBER OF REPUBLICAN SENATORS AND REPRESENTATIVES WHO ARE CALLING FOR BIPARTISAN ACTION TO STRENGTHEN THE INDIVIDUAL MARKET

Senate Majority Leader Mitch McConnell (R-KY): “Some Kind Of Action With Regard To The Private Health Insurance Market Must Occur. No Action Is Not An Alternative.” “‘If my side is unable to agree on an adequate replacement, then some kind of action with regard to the private health insurance market must occur,’ McConnell said. ‘No action is not an alternative. We’ve got the insurance markets imploding all over the country, including in this state.’” [Washington Post, 7/6/17]

Rep. Mark Meadows (R-NC): “I Don’t Think That Letting It Fail Is The Best Option, Even Though It Certainly Allows Additional Pressure To Happen.” “‘I don’t think that letting it fail is the best option, even though it certainly allows additional pressure to happen,’ said Rep. Mark Meadows, R-N.C., who is chairman of the House Freedom Caucus and close ties to the White House. ‘We can do better than that.’” [Washington Examiner, 7/31/17]

Rep. Mark Amodei (R-NV): Amodei Disagrees With President Trump, Believes The Individual Market Should Not Be Allowed To Fail. “Rep. Mark Amodei, R-Nev., rebuked Trump more directly. ‘No,’ he said when asked if he agreed with the president. ‘Clear-cut question — no.’” [Washington Examiner, 7/31/17]

Sen. John Thune (R-SD): “I Hope The President Will Continue To Make Those Payments.” [Kasie Hunt Tweet, 8/1/17]

Sen. Lisa Murkowski (R-AK): “The Senate Should Step Back And Engage In A Bipartisan Process To Address The Failures Of The ACA And Stabilize The Individual Markets.” “As I’ve been saying, the Senate should take a step back and engage in a bipartisan process to address the failures of the ACA and stabilize the individual markets. That will require members on both sides of the aisle to roll up their sleeves and take this to the open committee process where it belongs.” [Murkowski Statement, 7/18/17]

Sen. Lisa Murkowski (R-AK): “The Senate Should Take A Step Back And Engage In A Bipartisan Process To Address The Failures Of The ACA And Stabilize The Individual Markets.” “As I’ve been saying, the Senate should take a step back and engage in a bipartisan process to address the failures of the ACA and stabilize the individual markets. That will require members on both sides of the aisle to roll up their sleeves and take this to the open committee process where it belongs.” [Sen. Murkowski, 7/18/17]

Sen. Bill Cassidy (R-LA): “I Want To Stabilize The Insurance Market.” “Asked if a bipartisan stabilization bill would be needed if the current GOP bill fails, Sen. Bill Cassidy (R-La.) said, ‘I presume.’ He left the door open to supporting such a measure. ‘It depends on what it looks like, but I want to stabilize the insurance market,’ Cassidy said. ‘Families are paying too high premiums, so we’ve got to lower premiums.’” [The Hill, 7/13/17]

Sen. Bill Cassidy (R-LA): “Families Would Be Hurt” If Payments Not Made.” [Sahil Kapur Tweet, 8/1/17]

Sen. Ron Johnson (R-WI): The Senate Should “Bite The Bullet And Stabilize Those Markets.” “Sen. Ron Johnson (R-Wis.) has for months called for a bipartisan stabilization bill that would guarantee funding for ObamaCare payments, known as cost-sharing reductions, to insurers. Those payments are key to avoiding premium spikes and keeping insurers in the markets. Johnson said Tuesday that he hopes the GOP can pass something next week, but if not, ‘bite the bullet and stabilize those markets.’” [The Hill, 7/13/17]

Sen. John Hoeven (R-ND): “We Need To Stabilize The Health Insurance Market.” “Obamacare is failing and premiums continue to increase dramatically with some markets down to one or no insurance providers. That is why we need to make reforms to provide Americans with access to health care and affordable health insurance with more choice and competition. The CBO score of the Senate draft health care bill indicates that this legislation needs additional work to ensure that it meets this goal. Also, health care reform will be a process, not one bill. We need to stabilize the health insurance market to make it more competitive so consumers have access to better and more affordable health care policies. In addition, we want to ensure that low-income people have access to health care coverage either through Medicaid or a refundable tax credit that enables them to buy their own health insurance policy.” [Hoeven Statement, 6/27/17]

Sen. Lamar Alexander (R-TN): “The Senate Health Committee Has A Responsibility During The Next Few Weeks To Hold Hearings And Continue Exploring How To Stabilize The Individual Market.” “My main concern is doing all I can to help the 350,000 Tennesseans and 18 million Americans in the individual market who may literally have no options to purchase health insurance in 2018 and 2019. However the votes come out on the health care bill, the Senate health committee has a responsibility during the next few weeks to hold hearings to continue exploring how to stabilize the individual market. I will consult with Senate leadership and then I will set those hearings after the Senate votes on the health care bill.” [Alexander Statement, 7/18/17]

Sen. Lamar Alexander (R-TN): We Should “Approve The Temporary Continuation Of Cost-Sharing Subsidies For Deductibles And Co-Pays.” “‘While we build replacements, we want the 11 million Americans who now buy insurance on the exchanges to be able to continue to buy private insurance. Among the actions that will help are to… approve the temporary continuation of cost-sharing subsidies for deductibles and co-pays.’” [Politico Pro, 1/13/17]

INSURANCE COMPANIES AND STATE INSURANCE COMMISSIONERS HAVE WARNED THAT DEFAULTING ON COST SHARING PAYMENTS WILL INCREASE PREMIUMS, DESTABILIZE THE INDIVIDUAL MARKET, AND POTENTIALLY DISRUPT COVERAGE

National Association Of Insurance Commissioners: “Congress Must Act Quickly To Stabilize The Individual Health Insurance Marketplace Before They Adjourn For The District Work Period.” “As the latest attempt to repeal and replace the Affordable Care Act has failed, Congress must act quickly to stabilize the individual health insurance marketplace before they adjourn for the district work period. The window to act is rapidly closing, as rates must be finalized by mid-August and insurers are deciding whether to remain in this market or not. Without action, we anticipate more and more insurance companies pulling out across the country and significant premium rate increases in the majority of states. The National Association of Insurance Commissioners (NAIC) urges the Congress to take two immediate actions — fund CSR payments and market stability funding — to help shore up these markets. Cost-sharing reduction (CSR) payments are critical to the viability of the individual health insurance markets in a significant number of states and must be funded through 2018. Sufficient and sustained market stabilization funding for states to establish reinsurance programs or high-risk pool programs is also needed for long-term stability beyond 2018. These two actions alone would go a long way toward steadying the individual markets while ongoing debates over legislative replacement and reform options continue.” [NAIC, 7/28/17]

National Association of Insurance Commissioners: “We Write Today To Urge The Administration To Continue Full Funding For The Cost-Sharing Reduction Payments For 2017 And Make A Commitment That Such Payments Will Continue, Unless The Law Is Changed.” “On behalf of the nation’s state insurance commissioners, the primary regulators of U.S. insurance markets, we write today to urge the Administration to continue full funding for the cost-sharing reduction payments for 2017 and make a commitment that such payments will continue, unless the law is changed. Your action is critical to the viability and stability of the individual health insurance markets in a significant number of states across the country.” [Letter to Mick Mulvaney, 5/17/17]

Dan Hilferty, President and CEO, Independence Blue Cross: “We Firmly Believe Your Coverage Will Be There For 2018, If The Federal Government, Congress And President Commit To, Fund The Subsidies During An Interim Period Of Time.” “We firmly believe your coverage will be there for 2018, if the federal government, congress and president commit to, fund the subsidies during an interim period of time when we look at how we can fix the program long-term.” [CNN, 7/19/17]

Kurt Giesa, Practice Leader, Oliver Wyman Actuarial Consulting: “If payers do not gain clarity on funding of CSR payments soon, they will have to build that cost into their premiums.” “ … the current uncertainty regarding health reform and the ACA exchanges is making actuaries’ task as difficult as it has ever been … Two market influences, in particular, are complicating 2018 rate setting: the uncertainty surrounding continued funding of cost sharing reduction (CSR) payments and the question of how the relaxation of the individual mandate will impact enrollment and risk pools. Our modeling shows that this uncertainty, if it remains, could lead payers to submit rate increases between 28 and 40 percent, and more than two-thirds of those increases will be related to the uncertainty around CSR payments and individual mandate … If payers do not gain clarity on funding of CSR payments soon, they will have to build that cost into their premiums.” [Oliver Wyman Analysis, 6/14/17]

Dr. Mario Molina, Former CEO Of Molina Healthcare: ‘Don’t Let The Administration Fool You’ Into Thinking Insurers Are To Blame For Raising Premiums Instead Of Sabotage.” “The administration and Republicans in Congress want you to believe that insurers raising premiums for their plans or exiting the marketplaces all together are consequences of the design of the Affordable Care Act instead of the direct results of their own actions to sabotage the law. Don’t let them fool you.” [Op-Ed in US News & World Report, 5/30/17]

Dave Jones, California State Insurance Commissioner: “President Trump Appears On A Mission To Destroy Health-insurance Markets By Creating Instability Through His Own Actions And Thereby Depriving Millions Of Americans Of Health-care Coverage.” “President Trump’s first executive order directed federal agencies to ‘waive, defer, grant exemptions from, or delay’ ACA requirements. The IRS then announced reduced enforcement of the ACA health-insurance mandate, which in turn exposes health insurers to tremendous uncertainty as to who will be in the 2018 market. President Trump also threatens to cut the ACA assistance that consumers rely on to afford health care. In April Mr. Trump stated, ‘ObamaCare is dead next month if it doesn’t get that money.’ Just last month the nation’s insurance commissioners wrote to the Trump administration requesting assurances that cost-sharing reduction payments will continue, noting that this is critical to the ‘viability and stability of the individual marketplace.’ No such assurance has been provided. President Trump appears on a mission to destroy health-insurance markets by creating instability through his own actions and thereby depriving millions of Americans of health-care coverage.” [Letter to the Editor in Wall Street Journal, 6/27/17]

Marguerite Salazar, Colorado’s State Insurance Commissioner: The Trump Administration Threatens The Whole Market. “In Colorado, where most consumers continue to have multiple insurance choices, commissioner Marguerite Salazar said the Trump administration threatens the whole market. ‘My fear is it may collapse,’ she said.” [Los Angeles Times, 5/18/17]

John Naylor, CEO Of Medica In Iowa: “It Is Challenging To Stay Focused On Our Mission To Provide Access To High-quality Affordable Health Care When There’s Noise Around The System And A Lack Of Clarity Of Rules.” “‘It is challenging to stay focused on our mission to provide access to high-quality affordable health care when there’s noise around the system and a lack of clarity of rules,’ said John Naylor, chief executive of Medica, who called the amount of uncertainty being thrown at insurers at the moment unprecedented.” [Washington Post, 5/12/17]

Eric A. Cioppa, Superintendent of the Maine Bureau of Insurance: “If They Don’t Get A Subsidy, I Fully Expect Double-digit Increases For Three Carriers On The Exchanges Here.”“The uncertainty is extremely problematic. If they don’t get a subsidy, I fully expect double-digit increases for three carriers on the exchanges here.” [New York Times, 6/4/17]

Danielle Devine, Michigan Director of Operations, Meridian Health Plan: “The Uncertainty Over The Future Of The Subsidies Creates The Largest Reason For Significant Rate Increases.” “The political climate continues to make it difficult to price and the uncertainty over the future of the subsidies creates the largest reason for significant rate increases.” [Crain’s Detroit Business, 6/14/17]

Rick Notter, Director of Individual Business, Blue Cross Blue Shield of Michigan: “If We Don’t Have That Cost-sharing (Subsidy), We Have To Make Up The Difference And The Only Way For Us To Do That Is With A Higher Rate.” “If we don’t have that cost-sharing (subsidy), we have to make up the difference and the only way for us to do that is with a higher rate.” [Detroit Free Press, 6/14/17]

John Goodnow, CEO, Benefis Health System in Montana: Goodnow Said The Lifespan Of The Affordable Care Act Has Been Shortened Because Insurance Companies Are Pulling Out Of The Exchanges ‘because Of All The Fear That’s Been Created Over Funding.’ “Republicans are injecting instability into federal insurance marketplaces by suggesting lowering subsidies for people who buy coverage, and it’s a ‘slick trick’ to ensure the failure of the exchanges, the head of one of Montana’s largest hospitals said Thursday … Great Falls-based Benefis CEO John Goodnow said the lifespan of the Affordable Care Act has been shortened because insurance companies are pulling out of the exchanges ‘because of all the fear that’s been created over funding. ‘All you have to do is threaten to defund the subsidies,’ he said Thursday on a panel in Helena organized by the Montana Nurses Association to discuss the bill.” [Billings Gazette, 7/7/17]

Brad Wilson, CEO, Blue Cross Blue Shield of NorthCarolina: “The Failure Of The Administration And The House To Bring Certainty And Clarity By Funding CSRs Has Caused Our Company To File A 22.9 Percent Premium Increase, Rather Than One That Is Materially Lower.”“The failure of the administration and the House to bring certainty and clarity by funding CSRs has caused our company to file a 22.9 percent premium increase, rather than one that is materially lower. That will impact hundreds of thousands of North Carolinians.” [Washington Post, 5/26/17]

Teresa Miller, Pennsylvania Insurance Commissioner: “Instability Caused By Adverse Action From The Federal Government Will Do Nothing But Hurt Consumers Who Are Stuck In The Middle.” “Information provided by insurers shows the extent to which instability and changes would impact Pennsylvania’s 2018 health insurance rates. This proves what we already know — instability caused by adverse action from the federal government will do nothing but hurt consumers who are stuck in the middle. The 506,000 Pennsylvanians with Affordable Care Act-compliant plans in the individual market deserve single-digit rate increases like the ones most people will see if Congress and the Trump Administration choose not to risk consumers’ health and financial well-being by jeopardizing the stability of these markets.” [Press Release, 6/1/17]

Julie Mix McPeak, Tennessee State Insurance Commissioner: “Members Could Help Bring Immediate Stability And Potential Rate Relief For Our Consumers By Appropriating Cost-sharing Reduction Payments For The 2017 And 2018 Plan Years.” “As Congress continues to debate ACA reform efforts, Members could help bring immediate stability and potential rate relief for our consumers by appropriating cost-sharing reduction payments for the 2017 and 2018 plan years. Every dollar matters when Tennessee consumers are feeling like they need to choose between health insurance or groceries or mortgage payments and the Congress could take action that would pay immediate dividends.” [Statement, 7/7/17]

Julie Mix McPeak, Tennessee State Insurance Commissioner: “No One Feels Optimistic About The Market If CSRs Are Not Funded.” “I asked my colleagues at a meeting of insurance commissioners nationwide, and no one feels optimistic about the market if CSRs are not funded. We would prefer for funding of those cost-sharing reductions through ’19. Again figuring out who gets to make that decision has been tough for us as regulators …It’s that instability, that uncertainty, the insurers hate the most. They are going to price for that.” [The Tennessean, 5/12/17]

Kelly Paulk, Vice President, Product Strategy and Individual Markets, BlueCross BlueShield of Tennessee: Factoring In Whether The Cost-Sharing Reductions Are Paid And If The Coverage Mandate Will Be Enforced Will Raise Premiums By 21 Percent On Average. “Our 2017 rates are allowing us to earn a margin (profit) for the first time in four years and would have enabled us to propose only a small increase for 2018 to cover expected changes in medical and operating costs. However, we have to factor in two significant uncertainties — whether the federal government will fund cost-sharing reductions for low-income members and how the risk pool will change if the coverage mandate is not enforced … Combining those two factors leads to an average 21 percent rate increase.” [Blog Post, 6/30/17]

Mike Kreidler, Washington State Insurance Commissioner: “The Current Federal Administration’s Actions — Such As Not Committing To Reimburse Insurers For Cost-sharing Subsidies And Not Enforcing The Individual Mandate — Appear Focused Only On Destabilizing The Insurance Market.”“There is a great deal of uncertainty underlying our country’s health insurance system today and no state is immune. There are specific issues with our health insurance system that we need to address, such as the rising costs of prescription drugs and health care services. Yet, the current federal administration’s actions — such as not committing to reimburse insurers for cost-sharing subsidies and not enforcing the individual mandate — appear focused only on destabilizing the insurance market. Sadly, it’s the people in our communities and across the country who will pay the price.” [Statement, 6/19/17]